![]()

There cannot be meaningful democracy without transparency and without open public discourse of vital issues that affect the lives and livelihoods of the citizens

Joseph Stiglitz & Bruce Greenwald (2003), Towards a New Paradigm in Monetary Economics

Ceding the Power to Create Money to the Banking Sector

The history section explains that while commercial banks have acquired the power to create money from the state, they have not done so as a result of a democratic process by parliament. No government has ever decided to franchise out the power of money creation – in fact the only government to address the money creation issue passed a law that expressly forbade money creation by private banks.

The fact that money creation has been privatised by stealth is a huge democratic issue in its own right. How could this have been ignored for so long by so many successive governments? Ignorance amongst MPs, civil servants and economists is undoubtedly one reason. Vested interests and the way political parties are funded are likely to be others.

Even MPs that understand that there is a problem, and are not cowed by the idea of knocking the golden goose (more on that here) may simply opt to do nothing – scared that without public support their career is unlikely to benefit from rocking the boat.

By allowing commercial banks the power to create money the government has ceded a key power of government without any democratic debate as to whether it is in the countries best interest to have done so. Leaving this power to create money to the private sector creates a serious democratic deficit: a process that many would consider to be the sole prerogative of the state is in the hands of corporations who have no accountability to the wider public and whose interests are often at odds with those of society as a whole.

Consequences

Banks hold two key powers in today’s economy – they get to create money, and therefore decide the total level of both money and debt within an economy. Secondly, banks get to allocate this money to whichever sectors of the economy they wish to – and in the process shaping the economy.

With the five largest banks in the UK five banks accounting for the majority of all lending, there is a huge amount of power concentrated in very few hands, with next to no transparency or accountability to wider society. Unlike pension funds, banks are not required to disclose how they will use their customers’ money.

As 97% of the UK’s money supply is effectively held with banks, this allows them to allocate a larger sum of money than either the entire pension fund industry or the government. Consequently the UK economy is shaped by the investment priorities of the banking sector, rather than the priorities of society.

The democratic consequences of banks holding these two powers are discussed below.

Power

As described here, allowing banks the power to create money inevitably leads to economy which is inherently prone to booms, busts and financial crises. In short, banks create money without regard to how much is needed for the economy and society to operate effectively – for example, 90% of the money they create is put towards activities that do not contribute to the growth of the economy.

Lending money for unproductive purposes in inherently unsustainable, as it increases debt without increasing earnings. When the debt becomes too large people either default or sell assets to make repayments. Selling assets decreases their value, lowering wealth and consumption. Consumption is also reduced as people put more of their money towards debt repayments. Both effects slow growth in the economy creating the bust; if enough people default on their loans or assets prices fall too much then a financial crisis can ensue.

The government must then act as a fire-fighter – spending to get out of bank induced recessions, and bailing banks out during financial crises. All this money inevitably has to come from higher taxes and government borrowing.

The problem is that once banks realise that they are ‘too big’ or ‘too important’ to fail (normally after one of their number is bailed out) they start taking more risks, safe in the knowledge that if their bets pay off they will make more money than they otherwise would have (meaning bigger bonuses), but if their bets fail they will be bailed out by the government. As the financial crises increase in magnitude, the amount of money required for the bailouts also increases, forcing the government further and further into debt. If this goes on for long enough eventually the state’s ability to repay will be called into question:

In the Middle Ages … the biggest risk to the banks was from the sovereign. Today, perhaps the biggest risk to the sovereign comes from the banks. Causality has reversed

Andrew Haldane (2009), Banking on the State

Even if the ‘state’ survives, the cost of these bailouts diverts revenue from the activities that the government was elected to do, compromising its ability to fulfil its democratically mandated objectives. Furthermore, by allowing banks the power to create money the government has given up an important source of revenue – meaning higher taxes or lower spending than would otherwise be the case.

But what would we do without the banks’ taxes?

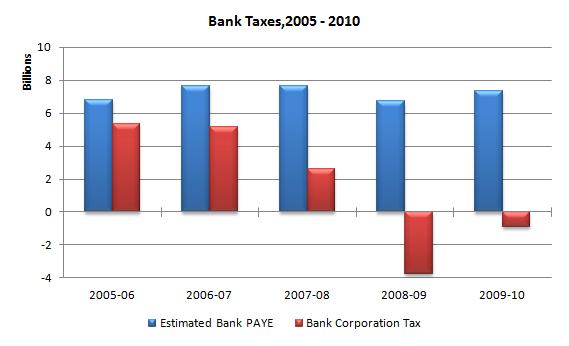

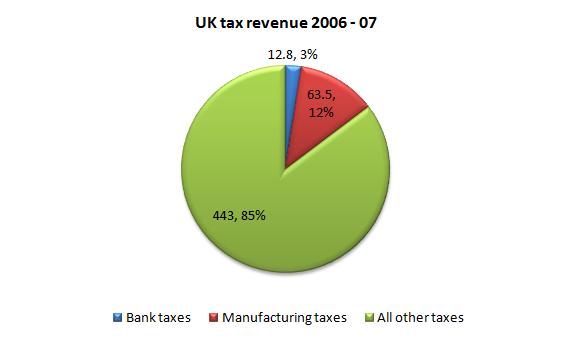

Of course, we are not just dependant on banks to create money, we are also dependant on them for taxes. Or are we? The chart below shows the Bank of England’s calculation of taxes paid by the banking sector:

That right: in 2008-09 and 2009-2010 banks actually paid no corporation tax at all. In fact they actually claimed back money paid in previous years. For those years when they actually did pay corporation tax (2005 – 08) their tax receipts were dwarfed by the manufacturing sector. Whereas the total tax paid by the banks was £12.8bn in 2006-07, tax paid by the manufacturing sector was around £63.5bn.

That right: in 2008-09 and 2009-2010 banks actually paid no corporation tax at all. In fact they actually claimed back money paid in previous years. For those years when they actually did pay corporation tax (2005 – 08) their tax receipts were dwarfed by the manufacturing sector. Whereas the total tax paid by the banks was £12.8bn in 2006-07, tax paid by the manufacturing sector was around £63.5bn.

If banks paying virtually nothing on their taxes was not bad enough they also receive an implicit subsidy from the tax payer. In 2007 this amounted to £10bn – more than they paid in corporation tax. By 2009 this had increase to over £100bn (for more see the subsidies section).

If banks paying virtually nothing on their taxes was not bad enough they also receive an implicit subsidy from the tax payer. In 2007 this amounted to £10bn – more than they paid in corporation tax. By 2009 this had increase to over £100bn (for more see the subsidies section).

Politicians and policy makers are misinformed about the true contribution of the banking sector. Without a proper understanding of the contribution and costs of the banking sector, how can politicians hope to act in the best interests of society as a whole?

http://www.positivemoney.org.uk/consequences/power-democracy/