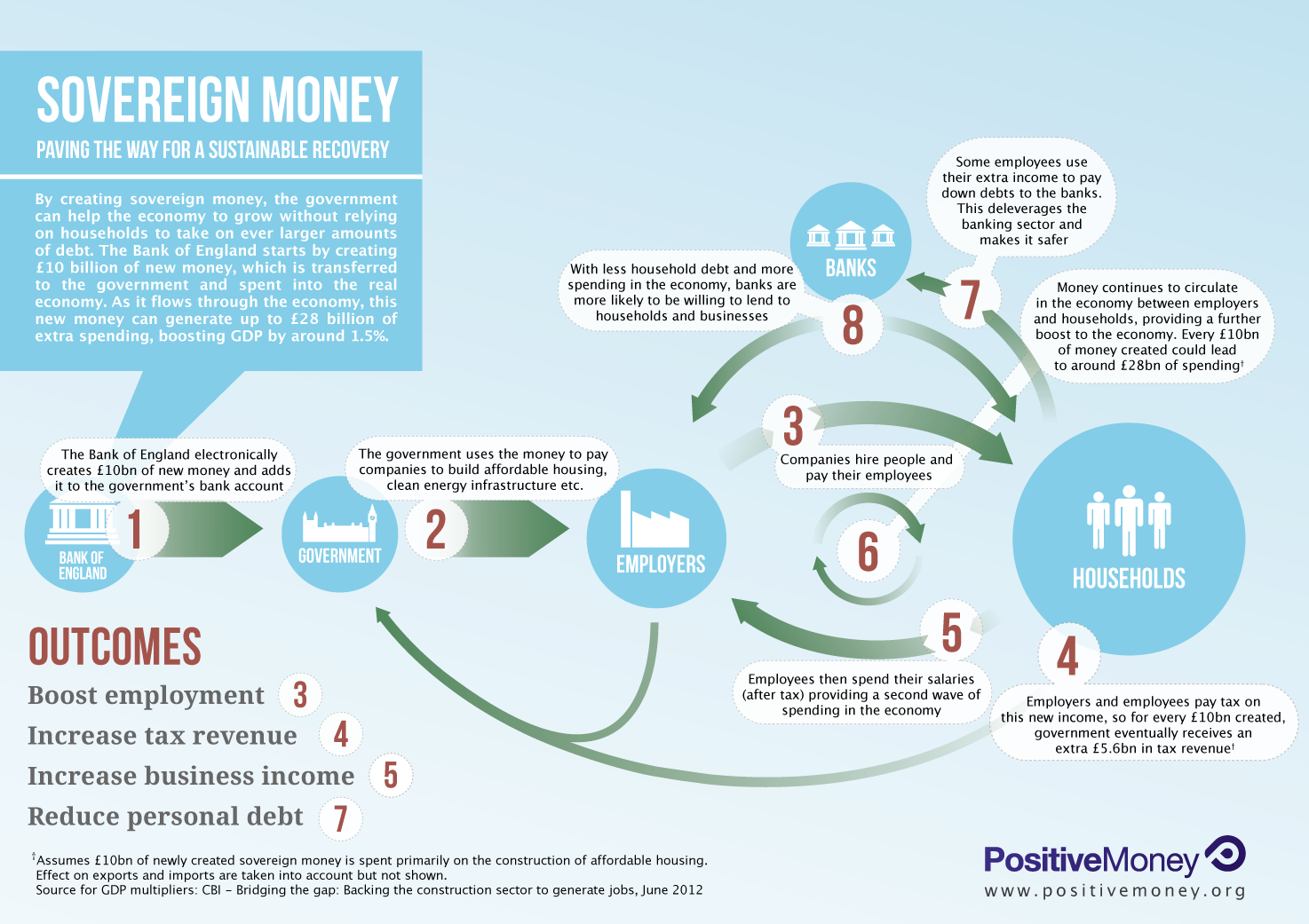

![]()

Speaker(s): Michael Kumhof

Chair: Professor Danny Quah

Recorded on 12 November 2013 in Old Theatre, Old Building, London School of Economics.

Michael Kumhof will discuss his 2012 paper on the Chicago Plan, a radical reform plan for the banking industry that would eliminate banks’ power to create money. Based on proposals developed by members of the Chicago School in the US in the 1930s, Kumhof’s plan represents the most far-reaching and decisive proposal to eliminate the risks associated with fractional reserve banking.

Michael Kumhof is deputy division chief of the Modelling Division at the IMF Research Department.

https://www.imf.org/external/pubs/ft/wp/2012/wp12202.pdf or click on the image:

1. The IMF (International Monetary Fund) paper advocates Debt-Free Money The IMF has released a paper in which the authors advocate Irving Fisher’s original 1930s proposals for banking reform, which remove the ability of banks to create money and which are the inspiration for Positive Money’s own proposed reforms. They’ve used state of the art economic modelling, and found strong support for the benefits of the proposals – reducing debt, making the banking system safer and stopping the instability in the money supply We’ve been in a state of mild shock since Saturday. We discovered one of the strongest advocates of full reserve banking in the institution where we would expect it least. The International Monetary Fund has released a paper “The Chicago Plan Revisited” that supports the proposals of Irving Fisher – those which are the basis for Positive Money’s proposals – using state of the art economic modelling. In their summary the authors Jaromir Benes and Michael Kumhof write: At the height of the Great Depression a number of leading U.S. economists advanced a proposal for monetary reform that became known as the Chicago Plan. It envisaged the separation of the monetary and credit functions of the banking system, by requiring 100% reserve backing for deposits.

Irving Fisher (1936) claimed the following advantages for this plan: (1) Much better control of a major source of business cycle fluctuations, sudden increases and contractions of bank credit and of the supply of bank-created money. (2) Complete elimination of bank runs. (3) Dramatic reduction of the (net) public debt. (4) Dramatic reduction of private debt, as money creation no longer requires simultaneous debt creation. We study these claims by embedding a comprehensive and carefully calibrated model of the banking system in a DSGE model of the U.S. economy. We find support for all four of Fisher’s claims. Here are few extracts from the paper: We therefore conclude that Fisher’s (1936) claims regarding the Chicago Plan, as listed in the abstract of this paper, are validated by our model. The effectiveness of countercyclical policy would be further enhanced under the Chicago Plan relative to present monetary arrangements. [B]ank runs can obviously be completely eliminated… It would lead to an instantaneous and large reduction in the levels of both government and private debt, because money creation no longer requires simultaneous debt creation… By validating these claims in a rigorous, microfounded model, we were able to establish that the advantages of the Chicago Plan go even beyond those identified by Fisher (1936)… One additional advantage is large steady state output gains due to the removal or reduction of multiple distortions, including interest rate risk spreads, distortionary taxes, and costly monitoring of macroeconomically unnecessary credit risks. Another advantage is the ability to drive steady state inflation to zero in an environment where liquidity traps do not exist… This ability to generate and live with zero steady state inflation is an important result, because it answers the somewhat confused claim of opponents of an exclusive government monopoly on money issuance, namely that such a monetary system would be highly inflationary. There is nothing in our theoretical framework to support this claim. And as discussed in Section II, there is very little in the monetary history of ancient societies and Western nations to support it either. The History of Monetary Thought in Section II is very interesting and certainly worth reading is the analysis of Government versus Private Control over Money Issuance (p 12). On the other hand, the historically and anthropologically correct state/institutional story for the origins of money is one of the arguments supporting the government issuance and control of money under the rule of law. In practice this has mainly taken the form of interest-free issuance of notes or coins, although it could equally take the form of electronic deposits. The historical debate concerning the nature and control of money is the subject of Zarlenga (2002), a masterful work that traces this debate back to ancient Mesopotamia, Greece and Rome. Like Graeber (2011), he shows that private issuance of money has repeatedly led to major societal problems throughout recorded history, due to usury associated with private debts. Zarlenga does not adopt the common but simplistic definition of usury as the charging of “excessive interest”, but rather as “taking something for nothing” through the calculated misuse of a nation’s money system for private gain. To summarize, the Great Depression was just the latest historical episode to suggest that privately controlled money creation has much more problematic consequences than government money creation. Many leading economists of the time were aware of this historical fact. They also clearly understood the specific problems of bank-based money creation, including the fact that high and potentially destabilizing debt levels become necessary just to create a sufficient money supply, and the fact that banks and their fickle optimism about business conditions effectively control broad monetary aggregates. The formulation of the Chicago Plan was the logical consequence of these insights. IMF Paper Backs Full Reserve Banking!

“The effectiveness of countercyclical policy would be further enhanced under the Chicago Plan relative to present monetary arrangements. [B]ank runs can obviously be completely eliminated… It would lead to an instantaneous and large reduction in the levels of both government and private debt, because money creation no longer requires simultaneous debt creation…”

Re-introduce Glass Steagall.

http://www.larouchepub.com/eiw/public/2012/2012_30-39/2012-31/pdf/23-25_3931.pdf